Tailoring your mortgage construction to your circumstances may allow you to repay your private home mortgage quicker. Find out how fastened price and floating price ANZ Home Loans work, to see which may be greatest suited to you. To discover out about different adjustments you would make to your private home mortgage to pay it off quicker and pay much less curiosity go to anz.co.nz/payitfaster

ANZ lending standards, phrases, circumstances, and costs apply. Interest charges and costs are topic to alter.

This materials is for info functions solely. We suggest searching for monetary recommendation about your scenario and targets earlier than getting a monetary product. To speak to one in every of our crew at ANZ, please name 0800 269 296, or for extra details about ANZ’s monetary recommendation service or to view our monetary recommendation supplier disclosure assertion see anz.co.nz/fapdisclosure ANZ Bank New Zealand Limited.

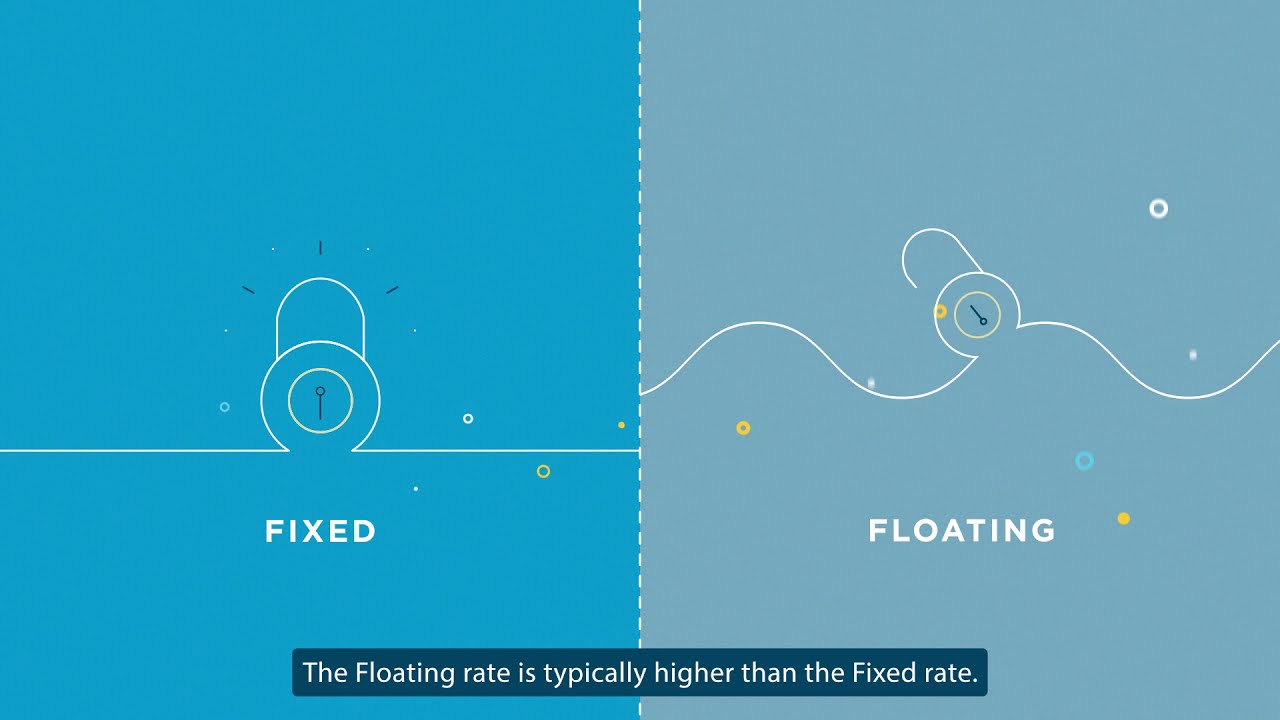

There are two commonplace ANZ Home Loan choices: Fixed price and Floating price.

They have some similarities like a most 30-12 months time period and no month-to-month charges. But, they’ve two large variations.

The first distinction is the rate of interest. Fixed means you lock in an rate of interest, for a set time. During that point, your reimbursement quantity stays the identical. Floating means your rate of interest will not be locked in, so it goes up or down in step with market adjustments, as do your reimbursement quantities. The Floating price is usually increased than the Fixed price.

And that is due to distinction two – the flexibleness to make further repayments. If reasonably priced, making further repayments may assist repay a mortgage quicker and should imply much less curiosity over the lifetime of the mortgage. With a Floating price, you’ve got the flexibleness to make further repayments everytime you like, with no further prices. With a Fixed price you may make one further reimbursement of as much as 5% of the present mortgage quantity annually of your Fixed price interval. Any further and you might be charged Early Repayment Recovery which is the loss we incur if you happen to repay some or your entire mortgage early throughout a Fixed price interval. Talk to us first, we may give you indication of the Early Repayment Recovery we’ll cost.

Many prospects select to place the bulk or all of their mortgage on a Fixed price as a result of the charges have been decrease, they usually like the knowledge of figuring out what their repayments shall be. They typically break up their mortgage throughout completely different Fixed price durations, to attempt to handle the danger of market adjustments. Customers who select to place a few of their mortgage on a Floating price like the knowledge of creating common repayments, however need the flexibleness to pay extra once they can. They may very well be anticipating some more money like a bonus that they need to put straight in the direction of their mortgage.

We know circumstances can change and it’s about what works greatest for you. The quicker you repay your mortgage, nevertheless, the much less you’ll pay in curiosity over the lifetime of your mortgage.

And if you happen to actually need to give attention to paying your private home mortgage off quicker there’s yet one more possibility.

Watch our video on Flexible Home Loans to search out out extra…

If you’ve got any questions, speak to us at the moment.

source

{kind=link}