Find out why paying off your home loan quicker could imply you’ll pay much less curiosity in the long run. To learn how you can make modifications to your home loan to pay it off quicker and pay much less curiosity go to anz.co.nz/payitfaster

ANZ lending standards, phrases, circumstances, and charges apply. Interest charges and charges are topic to vary.

This materials is for data functions solely. We suggest searching for monetary recommendation about your scenario and objectives earlier than getting a monetary product. To discuss to considered one of our crew at ANZ, please name 0800 269 296, or for extra details about ANZ’s monetary recommendation service or to view our monetary recommendation supplier disclosure assertion see anz.co.nz/fapdisclosure ANZ Bank New Zealand Limited.

This video will clarify how curiosity works and why paying your home loan again quicker could imply you’ll pay much less curiosity over the lifetime of the loan .

For most home loans the repayments typically cowl two issues:

Paying again the principal – the quantity borrowed and paying again the curiosity – the price of borrowing that cash.

Understanding how one can handle repayments might impression how a lot curiosity is paid over the lifetime of the loan.

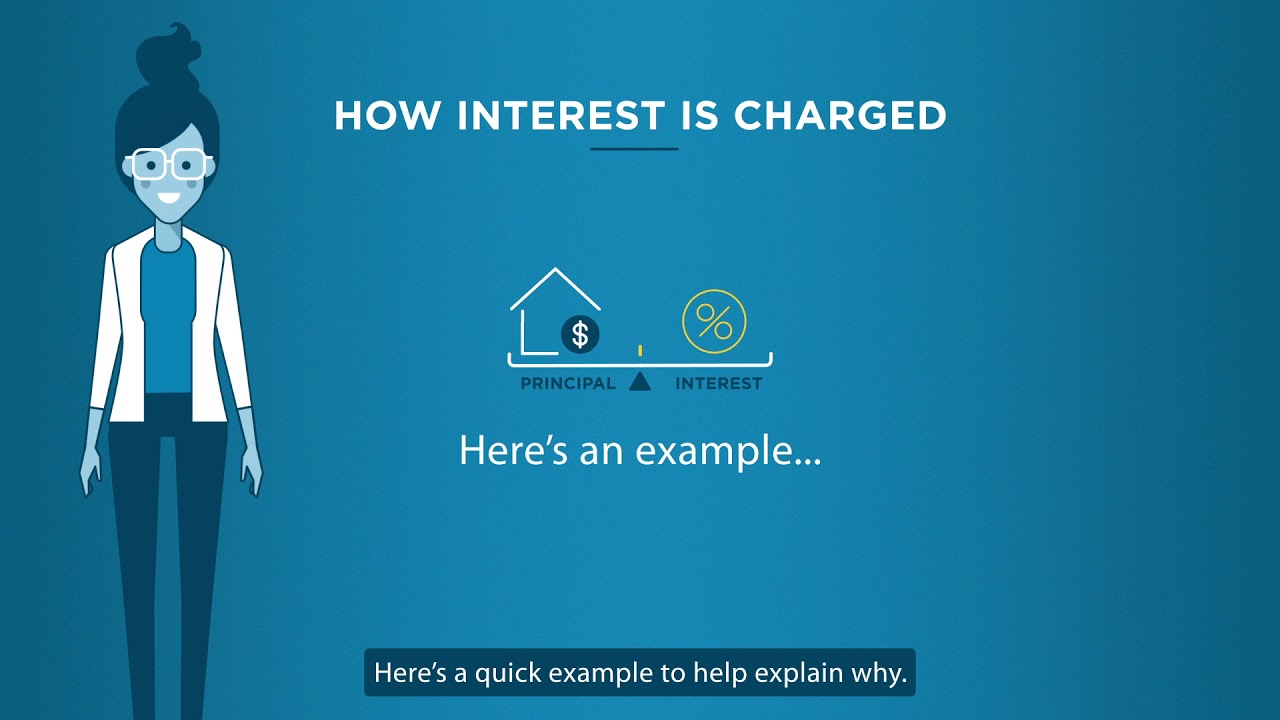

There are 3 components in understanding how the curiosity a part of every compensation works: the rate of interest; the way it’s calculated; and the way it’s charged.

Generally, the decrease the rate of interest the much less curiosity you are charged. But there are completely different loan sorts and rates of interest to select from, relying on your scenario and objectives. Remember – a home loan is a protracted-time period dedication and over time the market will fluctuate, that means rates of interest will too.

What many individuals don’t realise is that curiosity is calculated every day. So every single day you’ve a decrease loan stability counts. It’s a good suggestion to assessment how typically repayments are made and once you begin making them.

When folks first get a home loan, many are stunned to see how a lot of their compensation goes in direction of the curiosity value in comparison with their principal.

Here’s a fast instance to assist clarify why. Say you’ve borrowed $400,000, at 4% p.a. for a time period of 30 years. The weekly repayments can be set at about $440. Your very first compensation of $440 would go in direction of about $307 of curiosity. The remainder of your $440 compensation would go in direction of your principal, which reduces your loan stability. As your loan stability reduces over time, you’re charged much less in curiosity which suggests you pay extra in direction of the principal with every $440 compensation.

This is why rising compensation quantities – even by just a bit – might have a big effect. By rising compensation quantity this helps pay extra in direction of the principal, which might cut back the loan stability quicker.

Our repayments calculator has a software on the facet that allows you to see the curiosity you can keep away from paying by rising the compensation quantity.

Don’t fear in the event you’re not ready to extend your repayments in the mean time. How you handle your loan could change as your life modifications, and paying extra at instances once you’re in a position to might nonetheless make a giant distinction.

With mounted charge home loans it’s possible you’ll be charged to extend your repayments, so discuss to us first earlier than you ask to make any modifications.

We know circumstances change and it’s possible you’ll have to assessment your home loan’s construction. We’re right here to help you alongside the way in which.

Watch our different movies to see the completely different home loan constructions.

If you’ve any questions, discuss to us as we speak.

source

{kind=link}